Here are Some $$$ Tips for National Financial Literacy Month

Photo by: Kertlis/Getty Image

The month of April is dedicated to financial literacy, and having knowledge is essential for financial success.

Financial literacy can have an impact on everything from the amount of money saved to the quantity of debt incurred.

According to Investopedia, the term financial literacy is defined as the ability to understand and effectively use various financial skills, including personal financial management, budgeting, and investing.

It’s the foundation of your relationship with money, and it is a lifelong journey of learning. For many, the situation is dire.

According to a January survey by Bankrate, more than half of Americans can’t handle a $1,000 emergency bill with their savings. Salary Finance reports that roughly 20% of employees run out of money before their next paycheck. This is up from 15% the previous year.

Here are four crucial financial skills to master to achieve financial literacy.

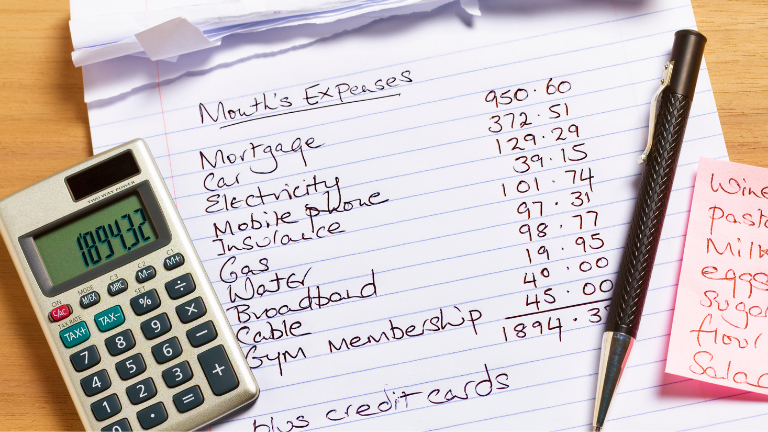

- Begin keeping track of your monthly expenses.

We all spend money, right? One helpful tip you can easily start your financial literacy journey is to jot it down in a notepad or on a mobile app every time you spend money.

Photo by: Peter Dazeley/Getty

In one’s everyday life, unexpected things can happen and we can lose track of how much money we are actually spending. So, it can become extremely easy to forget about this, so stay vigilant.

This is the foundation of your financial planning and most importantly: budgeting.

- Determine which expenses are constant and which are changeable.

To make things easier, you can look at your finances in two ways: constant expenses vs. changeable expenses.

Rent, mortgage, auto payments, an energy bill, a water bill, and student loan payments are examples of constant expenses.

Groceries, pet supplies, haircuts, concert tickets, and other expenses that fluctuate month to month and come and go are examples of changeable expenses.

After you analyze how much you are spending, begin to place each expense into these two categories.

- Add the totals together.

Once you figure out which expenses are constant or changeable, you need to calculate how much you spend on average each month.

Photo by: Marko Geber/Getty

Keep track of this information for the next three months. This will save you from any financial worry you might not have caught otherwise.

- Examine your variable costs.

Let’s be truthful, most people overspend.

To avoid overspending, you must decide and determine which element of your monthly spending brings you the most pleasure and whether the prices are justified.

And begin narrowing down which expensive you can genuinely do without. Once you come to terms with which changeable expensive you want to splurge on and what you can cut, follow through with that mindset.

- Begin to add money into your savings.

Know that you have analyzed how much money you’re spending, making changes to cut out any unnecessary spending, next what you’d need to do is begin to save.

To save money, you’d want to set aside a percentage from each of your earnings and place the money into your savings.

Photo by: Richard Drury/Getty

If you can make this one exercise a habit, it will pay off and save you many financial problems that you are able to control throughout your life.

There are many cases when unexpected financial instances where you need to spend a significant amount of money such as job loss, car repairs, house repairs, hospital bills, and more. Starting to save and having a savings account can save you in the long run.

- Create a budget.

For the final step to begin your financial literacy journey, you should begin to cut your expenses as soon as possible.

Next, you’d have to decide how much money you want to put aside every week or every two weeks.

Photo by: Peter Dazeley/Getty

The money you have leftover is how much you can live on.

Effective budgeting necessitates being honest with yourself and creating a strategy that you can stick to. The more time and effort you put into your budget today, the more likely you are to develop a long-term saving habit.

Tell us your favorite financial tips that you’ve learned down below!